Glass has crossed a threshold. What was long regarded as a passive, protective substrate is now performing as a strategic engineering material in some of the most demanding applications in aerospace, defence, and medical device development. Advanced compositions, precision processing, and nanostructuring have redefined what glass can deliver, solving problems that composites, silicon, and polymers simply cannot address at scale. For product development managers navigating a fast-moving landscape of material options, understanding which glass innovations are mature enough to specify, and which are approaching readiness, is now a direct competitive advantage.

Table of Contents

- Transformative roles for glass in 2026: Context and market outlook

- Cutting-edge glass innovations in aerospace and defence

- Medical and electronics: Ultra-thin, smart, and advanced glass solutions

- Advanced compositions and processing: Nanostructured, liquid-like and high-performance glass

- What most managers miss about deploying advanced glass

- Solutions and next steps: Partnering for your glass innovation roadmap

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Glass enables new frontiers | Breakthrough advances now position glass at the core of aerospace, defence and medical innovation. |

| Specialised glass types lead | Ultra-thin, nanostructured, athermal, and liquid-like glasses support miniaturised, safer, and more precise devices. |

| Selecting glass is strategic | Early collaboration and holistic testing are critical when integrating new glass technologies into advanced products. |

| Performance outpaces tradition | Modern glass combines unmatched properties with engineering rigour, moving well beyond legacy materials in many applications. |

Transformative roles for glass in 2026: Context and market outlook

Glass has become a core enabler in high-value sectors, not merely a packaging or optical component. Three distinct market trajectories confirm this shift and give product leaders clear signals for where investment in glass knowledge pays off.

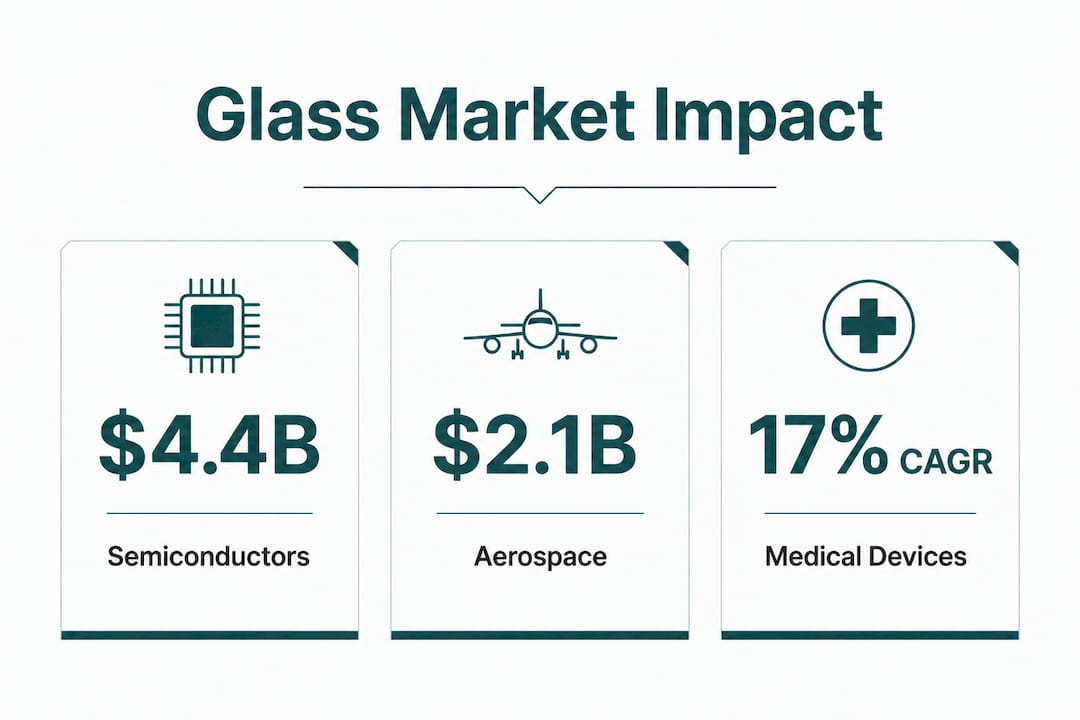

The semiconductor industry is driving one of the most significant transitions. Glass core substrates for advanced packaging are forecast to reach US$4.4 billion by 2036, growing at a CAGR of 14.2%. That growth is not speculative. AI and high-performance computing packages demand signal integrity, low loss, and dimensional stability that organic laminates cannot consistently provide at next-generation frequencies.

In aerospace, the aircraft transparency market is valued at $1.58 billion in 2026 and projected to reach $2.13 billion by 2030, reflecting a CAGR of 7.8%. Lightweighting requirements, bird-strike safety standards, and smart glass integration are all accelerating this figure. For medical and wearable applications, the ultra-thin glass market stands at $26.59 billion in 2026, with the medical segment accounting for approximately 25% and growing at a CAGR of 9.89%.

| Market segment | 2026 value | Growth rate | Key driver |

|---|---|---|---|

| Glass core substrates | Part of $4.4B (by 2036) | 14.2% CAGR | AI/HPC packaging needs |

| Aircraft transparencies | $1.58B | 7.8% CAGR | Safety, lightweighting |

| Ultra-thin glass (medical) | ~$6.6B (25% of $26.59B) | 9.89% CAGR | Wearables, miniaturisation |

These numbers represent procurement decisions already being made. The organisations positioned to act are those whose product development teams understand the performance benchmarks glass now achieves, specifically in electrical properties, thermal stability, mechanical endurance, and optical transmission.

Having set the stage for glass as a material transforming critical sectors, let’s break down the most significant application trends shaping 2026.

Cutting-edge glass innovations in aerospace and defence

Aerospace and defence applications remain the most demanding proving grounds for glass performance. The standards set in these sectors routinely migrate into medical and electronics supply chains, making early familiarity with aerospace-grade developments strategically valuable.

Aircraft transparencies have evolved well beyond conventional laminated windscreens. Current procurement trends reflect demand for smart glass, bird-strike laminated glass, and advanced heated systems that integrate suspended particle device (SPD) layers for anti-glare control and electrochromic switching. These systems reduce pilot fatigue and cockpit thermal load without adding significant mass. Simultaneously, laminated constructions that meet bird-strike certification requirements are being refined to achieve lower total weight while retaining structural integrity at speed and altitude.

In defence optics, three material categories dominate precision imaging and sensing: chalcogenide glass, sapphire, and zinc sulphide/zinc selenide (ZnS/ZnSe). Sourcing decisions in this space require understanding their distinct trade-offs. Chalcogenide glass transmits across 3 to 14 microns in the infrared, making it indispensable for thermal imaging, missile seekers, and night-vision systems. Sapphire, rated Mohs 9 and stable up to 1000 degrees Celsius, offers transmission from 150 nanometres through 5.5 microns and resists abrasion in exposed dome and window applications. ZnSe and ZnS serve as mid-wave and long-wave infrared windows where sapphire’s transmission falls short.

| Material | IR range | Hardness | Key application |

|---|---|---|---|

| Chalcogenide glass | 3–14 µm | Moderate | Thermal imaging, seekers |

| Sapphire | 150 nm–5.5 µm | Mohs 9 | Domes, exposed windows |

| ZnSe/ZnS | 1–20 µm | Lower | Broadband IR windows |

| Low-CTE glass | Visible/NIR | High stability | Lithography, targeting |

For imaging systems, satellites, and airborne targeting platforms, low thermal expansion glass with precisely controlled homogeneity is essential. Even minor thermal gradients in mirror substrates or lens mounts generate wavefront errors that degrade system performance. Low-CTE materials maintain dimensional stability across the operating temperature range these platforms encounter, from ground-level heat to upper-atmosphere cold. Specifications routinely call for coefficient of thermal expansion values below 0.5 parts per million per degree Celsius, with tight homogeneity requirements across large apertures.

You can review a detailed breakdown of aerospace glass solutions and understand how these materials translate into specific product geometries and coatings. For display and HMI applications in defence platforms, the requirements for display glass for defence environments include scratch resistance, extended temperature ranges, and specific anti-reflection treatment.

Pro Tip: Engage your glass supplier at the concept stage, not at drawing release. Early material dialogue allows your team to align CTE, thickness tolerances, and coating compatibilities before the system architecture is locked. This approach alone can prevent months of qualification rework.

Key considerations when specifying aerospace and defence glass:

- Verify transmission curves across your full spectral range, not only at peak wavelengths

- Confirm CTE data at operational extremes, not just room temperature

- Understand the coating stack in full before finalising housing or bonding design

- Assess surface quality standards using scratch/dig designations appropriate to the application

With aerospace and defence setting the benchmark for performance and reliability, let’s see how innovations are manifesting in medical and electronics glass.

Medical and electronics: Ultra-thin, smart, and advanced glass solutions

Ultra-thin glass (UTG) is fundamentally changing what is achievable in medical device design and wearable electronics. At thicknesses below 0.1 millimetres, UTG maintains excellent flexibility, scratch resistance, and chemical resistance, properties that polymers approximate but cannot match across the service life of a clinical-grade device. Anti-microbial coatings applied to UTG surfaces are integral to infection control in point-of-care diagnostics and surgical imaging systems.

Fusion-drawn and float-processed glass enables the large-area uniformity required for wearable displays and flexible medical sensors. These manufacturing routes achieve surface roughness values that support functional coatings reliably without the post-processing steps that add cost and risk in high-volume production. The result is a substrate that can carry anti-reflection, anti-fingerprint, and electrically conductive layers in a stable, reproducible stack.

For electronics, glass core substrates outperform organic and silicon alternatives in signal speed, insertion loss, and dimensional stability under repeated thermal cycling. These properties are directly relevant for AI accelerator packaging and high-bandwidth memory stacks where panel warpage during processing causes yield losses at scale. The transition from organic build-up to glass core is not trivial, but organisations that manage it gain significant headroom for next-generation interconnect density.

Understanding medical glass terminology is a practical starting point for engineering teams entering this space. The glass specification guide provides a structured framework for aligning material selection with regulatory and performance requirements.

Qualifying new glass for medical or electronic use follows a structured sequence:

- Define performance requirements in full, including mechanical, optical, thermal, chemical, and regulatory constraints

- Conduct material screening against published datasheets, with shortlisting of two to three candidates for testing

- Engage suppliers early to discuss surface finish, coating options, micro-defect tolerances, and sampling lead times

- Execute application-specific validation covering accelerated life testing, environmental exposure, and interface compatibility

- Plan scale-up deliberately, with yield targets, inspection protocols, and agreed defect classification criteria from the outset

Pro Tip: Negotiate surface finish specification, micro-defect classification limits, and functional coating requirements before the first prototype batch. Discovering mid-qualification that your supplier’s standard product does not meet your defect acceptance criteria adds substantial programme risk.

The diversity of application spaces demands ever more specialised glass chemistries and structures. Next, we will examine the most advanced compositions and processing techniques reshaping what glass can do.

Advanced compositions and processing: Nanostructured, liquid-like and high-performance glass

The boundaries of what glass can deliver are being actively extended through nanostructuring, novel phase-separation chemistries, and liquid-like glass formulations. These are not laboratory curiosities. Several are approaching specification-ready status for aerospace and medical applications in 2026.

Nanostructured lithium-aluminosilicate glass-ceramics represent a particularly significant advance. Research published in 2025 demonstrates enhanced crack resistance and self-healing behaviour achievable through low-temperature, short-duration formation processes. The self-healing mechanism, driven by dendritic phase structures, suppresses crack propagation under cyclic mechanical loads. This is directly relevant for aerospace transparencies and medical device housings that experience repeated vibration and pressure cycling.

Key benefits and application areas for advanced glass compositions:

- Lithium-aluminosilicate glass-ceramics: Improved fracture toughness, thermal stability, lightweight compared to engineering ceramics

- Chalcogenide glass formulations: Broadband IR transmission, laser power delivery without thermal damage

- Liquid-like glass structures: Consistent performance through repeated thermal cycling for sensor and imaging components

- Phase-separated glasses: Tunable porosity and refractive index for optical filters and bioactive coatings

Liquid-like chalcogenide glass is emerging as a material of significant interest for advanced sensing and directed-energy systems. Recent research confirms 91% mid-infrared transmission with reliable performance across repeated thermal cycling events, a combination that has not been achievable in conventional fibre or bulk chalcogenide forms. Laser power delivery through such materials opens possibilities in surgical laser delivery, target designation, and standoff chemical detection.

“Advanced glass formulations are not arriving as drop-in replacements. They require system-level integration planning, supplier collaboration from concept, and meticulous validation at every transition from laboratory to production.”

Understanding the glass fabrication processes that underpin these materials is valuable context when evaluating supplier capability. Not every precision glass manufacturer has the equipment or process control for nanostructured ceramics or UTG fusion drawing.

What most managers miss about deploying advanced glass

Most product development teams underestimate the systemic nature of switching to an advanced glass material. The material change itself is rarely where projects stall. The delays accumulate in qualification planning, metrology gaps, and interface mismatches that were not anticipated because the glass was treated as a commodity input rather than a system-critical component.

Empirical data confirms that glass is enabling measurable gains in AI and HPC scaling, infrared imaging superiority, and aero-structure weight reduction. But accessing those gains requires organisational readiness, not just a purchase order.

The total cost of transitioning to advanced glass is consistently underestimated. New defect modes, different cleanliness requirements, altered bonding processes, and customer-imposed qualification activities all carry cost and schedule consequence. Engineering teams that treat advanced glass adoption as a material substitution are the ones that encounter these costs mid-programme, at the worst possible time.

The most under-appreciated failure mode we observe is the absence of a three-way conversation between engineering, quality, and the glass supplier at project conception. By the time quality teams understand the defect criteria and the supplier understands the application stresses, drawing revisions and re-qualification cycles have consumed months. This is avoidable with structured early engagement.

“High-performance glass shifts the innovation bottleneck: it is rarely the material, but decision velocity and integration. The value accrues to those who plan for new testing, not just those who buy new glass.”

Sound optimising glass sourcing practice begins with treating the supplier as a development partner rather than a catalogue vendor. Organisations that do this consistently qualify faster, achieve better first-article yields, and generate proprietary performance advantages that competitors cannot easily replicate.

Solutions and next steps: Partnering for your glass innovation roadmap

Navigating the breadth of advanced glass technologies requires more than a shortlist of materials. It requires a supplier with deep process knowledge, meticulous quality systems, and the flexibility to co-develop solutions tailored to your specific application constraints.

At Glass Precision, we work directly with product development teams in aerospace, defence, and medical equipment manufacturing to align material selection, surface specification, and coating requirements to programme objectives from the outset. Our technical team supports requirements definition, supplier dialogue, and qualification planning to reduce programme risk and accelerate time to first article. Access our specifications guide for engineers for a structured approach to documenting your glass requirements, or review our critical industry fabrication capabilities to understand the process controls we maintain for precision and large-volume programmes.

Frequently asked questions

What is the difference between ultra-thin glass and traditional glass for medical devices?

Ultra-thin glass offers greater flexibility, superior scratch and chemical resistance, and supports advanced coatings such as anti-microbial layers, making it substantially more suitable for modern medical devices and wearables than conventional glass substrates.

Why are chalcogenide and sapphire glasses preferred in defence optics?

Chalcogenide glass enables precise infrared imaging across 3 to 14 microns, while sapphire provides Mohs 9 hardness and thermal stability up to 1000 degrees Celsius, with both excelling in the durability and transmission demands of defence environments.

What are the main engineering challenges of using advanced glass in high-frequency electronics?

Key challenges include matching CTE, managing warpage, and via-fill reliability in glass core substrates during panel-scale processing for high-speed, low-loss signal applications.

How is glass performance tested for aerospace transparency and defence standards?

Performance is assessed through impact, bird-strike, and thermal cycling testing, alongside optical clarity measurement and coated-surface durability evaluation, with smart glass systems also assessed for response consistency under varied environmental conditions.

How does nanostructuring improve glass-ceramics in extreme environments?

Nanostructuring delivers enhanced crack resistance and self-healing capability, enabling glass-ceramics to maintain structural integrity under dynamic mechanical loads and rapid thermal cycling typical of aerospace and critical medical deployments.

Recommended

- Top glass solutions for aerospace: strength, clarity, precision – Precision Glass

- Medical glass terminology explained for device engineers – Precision Glass

- Glass in electronics: Performance, reliability and procurement insights – Precision Glass

- Advanced glass specifications: Guide for engineers and buyers – Precision Glass

- Filament-based prototype examples for high-quality 3D printing